Earnings-related pensions help you in different life situations. In this section you will find information on the various pension benefits available for different life situations, how your pension amount is calculated and when and how you can claim the pension.

The most common earnings-related pension is the old-age pension. But earnings-related pensions provide for you also if you become disabled or if a wage earner in your family dies. You can retire on a partial old-age pension when you turn 62.

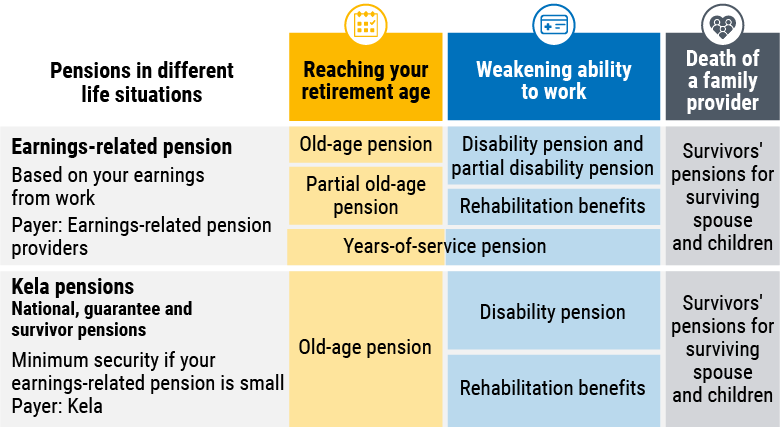

Most pensions are earnings-related pensions. You earn your earnings-related pension by working or by being a self-employed person. Earnings-related pensions are paid by pension providers. If your earnings-related pension is small, you may have a right to receive a national or a guarantee pension paid by Kela.

To find the general instructions on how to claim a pension from Finland or abroad, go to the section Claim your pension.

Earnings-related pension benefits based on your work are paid out one at a time

You can only receive one work-related pension benefit at a time (such as an old-age pension, partial old-age pension, disability pension, or years-of-service pension) as these benefits are mutually exclusive. For example, you cannot get both a partial old-age pension and a (partial) disability pension at the same time. An exception is the survivor’s pension, which you can receive in addition to another earnings-related pension benefit.

Pension benefits in brief

Old-age pension

An earnings-related pension provides you with a secure income after your working life. You can retire at the earliest when you reach the statutory retirement age for your age group. Your year of birth therefore determines when you can retire. The older you are when you retire, the higher your pension will be.

Partial old-age pension

When you are on a partial old-age pension, you can decide yourself how much you want to work. You can qualify for a partial old-age pension once you reach the minimum retirement age for your age group. If you were born in 1964, you must have turned 62. If you were born in 1965 or later, you can draw a partial old-age pension up to three years before your own retirement age. The part of your pension that you take out early (before you reach your retirement) age will be permanently reduced.

Rehabilitation or disability pension

Rehabilitation is always a primary alternative if your work ability is reduced. Rehabilitation can help you continue working.

The disability pension is an option only once your illness, handicap or injury reduce your working ability in the long run, for more than one year.

Read more about rehabilitation

Read more and apply for a disability pension

Years-of-service pension

You may qualify for a years-of-service pension at the age of 63 if you have worked for at least 38 years in a job that requires great mental or physical effort and have a health condition that affects your ability to work.

Survivors’ pensions

The survivors’ pensions replace income that is lost when a family wage earner dies.

What strokes to take towards the end of your career?

Some aim for the shallow end and retire as soon as they reach their retirement age, others swim laps for a longer time, and some opt for floating aids. Make sure to dive into the different retirement options and understand what they mean for you personally. Explore the example calculations for Sarah’s pension.